A major reason for the weakening growth of the German economy, besides the global downturn, are the necessary investments to be made in the automotive industry. The low stocks and inability to invest amplifies the effect for car companies already struggling.

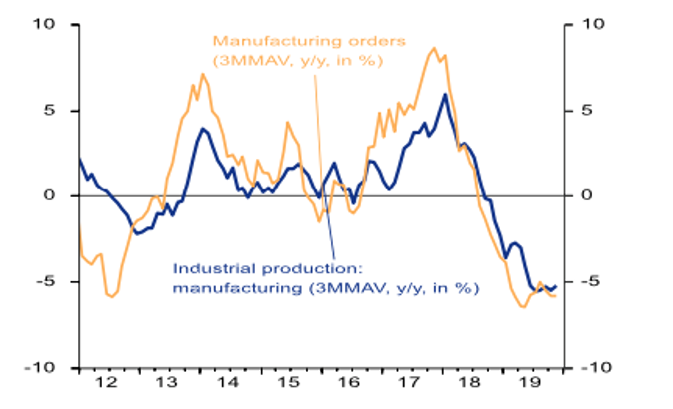

The so-called manufacturing orders showed a decline of -1.3 per cent over November 2019, bringing the year-to-date total to a whopping -6.5 per cent. In the same month, the industrial production by 1 per cent, but this did not help the industrial recession that has set in since the third quarter of 2018, to stop. German exports showed a decline of -2.3 per cent in November. This decline wiped out the 1.5 per cent growth over the month of December.

Expectations 2020

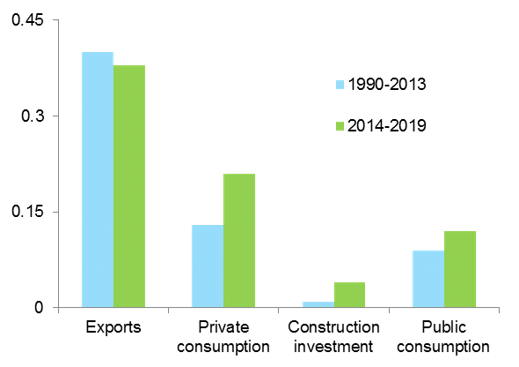

The avoidance of a recession in Germany over the whole of 2019 was solely due to a Solid growth in private consumption, government spending and construction investment. Those factors will therefore also have a significant effect on the growth for 2020, again estimated at 0.6 per cent.

A strong recovery in industrial production could boost growth. German exports are also expected to show (slight) recovery. But the weak position of the German automotive industry and the somewhat uncertain political situation in our eastern neighbour are causing that the economic situation will remain fragile for the time being. The rise in domestic consumption and government spending should offset the fall in exports, as shown in the figure below.

Fortunately for Germans, their labour market is still well balanced. However, we do see a drop in the number of open jobs and temporary workers in recent months. The unemployment rate is expected to rise by 1 basis point to 5.1% in 2020.

What does the German situation mean for the Netherlands?

All in all, then, it is a fragile balance on the other side of our border. Moreover, the trade war, the slowdown in the global economy, the coronavirus and still a variety of geopolitical risks are external factors that are driving the Putting even more pressure on German economy.

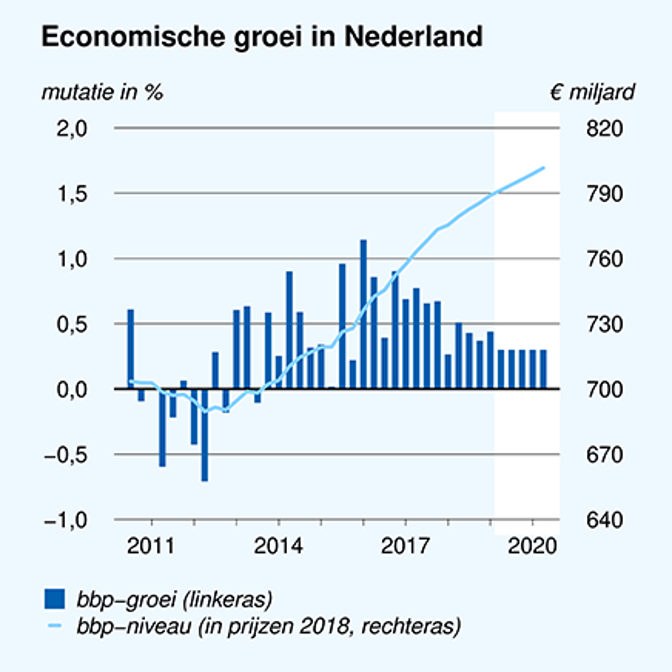

In the Netherlands, we certainly also see a flattening of growth, although not as severe as in Germany. Nevertheless, the Dutch economy is closely linked to the German economy. It is not for nothing that the saying goes, "When Germany sneezes, the Netherlands catches a cold". In slowdown, we will certainly also experience the effects of the flattening of the economy in Germany, but we do not yet have a cold.

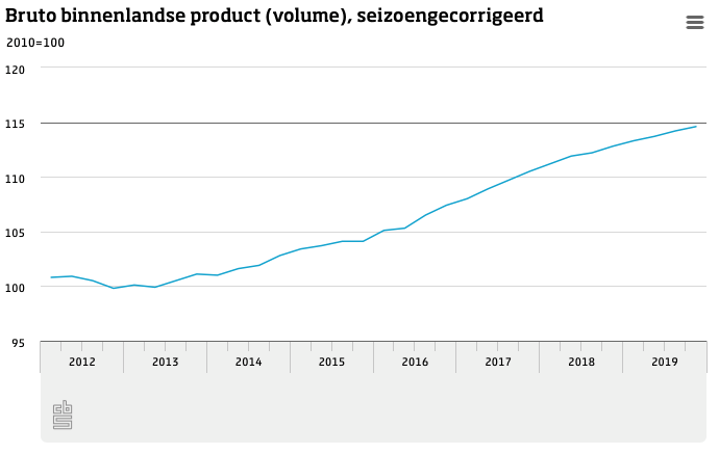

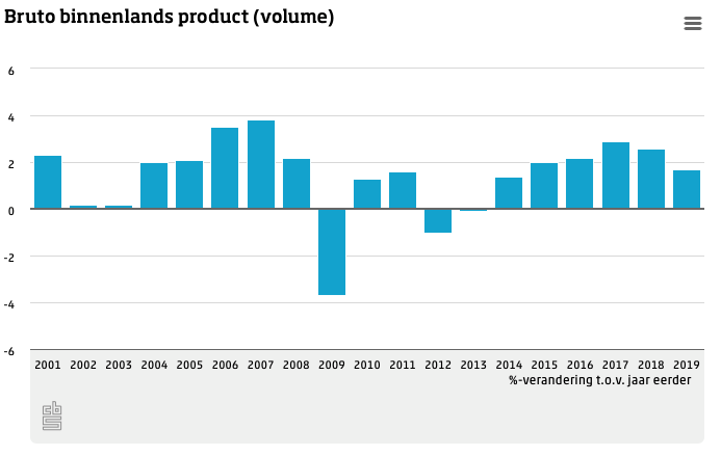

GDP growth in 2019 was still 1.7%.

In this graph, we can see that growth is levelling off. This growth is expected to flatten further in 2020. Rabobank's economists previously published the forecast that growth will average 1 per cent over the next decade. This is sharply lower than the past decade.

We can see the impact of slowing growth in the following:

- Increase in bankruptcies;

- Increase in unemployment;

- Decrease in government budget surplus.

In contrast, wages will rise further this year and inflation remains low. Compared to many other countries, the Dutch economy is stable though and usually endures economic recessions very well. So there is absolutely no reason to panic yet about the situation in Germany.