Shiverthe banks

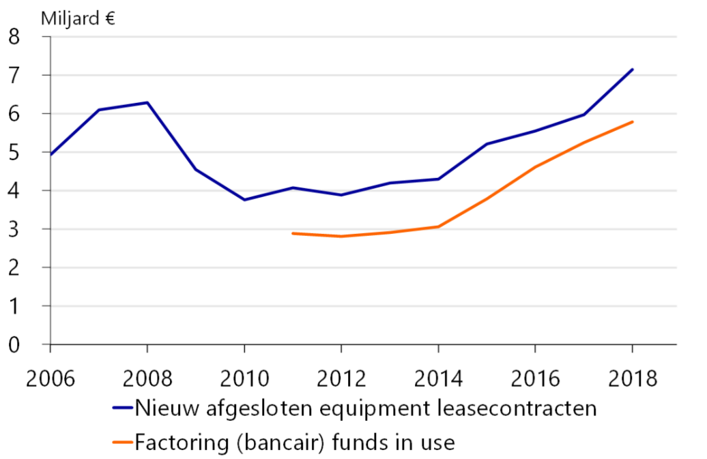

Since the last economic crisis, general banks have become increasingly reluctant to provide financing to SMEs. The outstanding amount of bank credit has already been declining since the end of 2012, according to CBS' Financing Monitor 2019. Although the major banks are still a major player in terms of loans, it appears to be very difficult for the average SME entrepreneur to attract working capital. And that while he desperately needs that working capital, for instance to finance the growth of his business or absorb seasonal peaks. But due to the lack of 'hard' collateral - and with the crisis still fairly fresh in their minds - the major banks are not at home.

Factoring fast-growing form of financing

The designated solution listens to the name factoring. Compared to 2018, factoring one of the fastest growing non-bank financing forms in 2019. In the past five years, the amount of financing through factoring even doubled, as shown in the picture below. Not surprisingly, dozens of new financiers in the Netherlands have jumped into the gap left by the major banks in recent years. These new kids on the block often offer two basic solutions: financing the entire receivables portfolio (traditional factoring) or buying one or more invoices (single invoice factoring).

Note: Includes mainly bank factoring. So the total factoring market is larger. Includes large companies.

Structural solution

In the first case - financing the entire accounts receivable portfolio - the SME transfers its invoices periodically, usually once a week. In return, it gets current account financing (advance payments) of 70 to as much as 90 per cent of the total invoice amount including VAT. The exact amount of the financing depends on several factors, including distribution of the number of customers, hardness of performance and whether the debtors are credit-insured. After the debtors have paid, the company receives the balance of the amount. This form of factoring offers a structural solution to a company's financing needs. Moreover, the cost is not much higher than that of an overdraft at the bank.

One-off credit requirements

In scenario two - selling one or more invoices - the entrepreneur 'sells' the invoice to the factoring company. He then immediately receives an amount of 90 to a maximum of 98% of the invoice amount paid out. The factoring company then runs the risk of non-payment. Therefore, the lender only accepts invoices relating to completed performance on creditworthy debtors. This form of factoring is a lot more expensive, but is ideally suited to filling one-off or temporary credit needs.

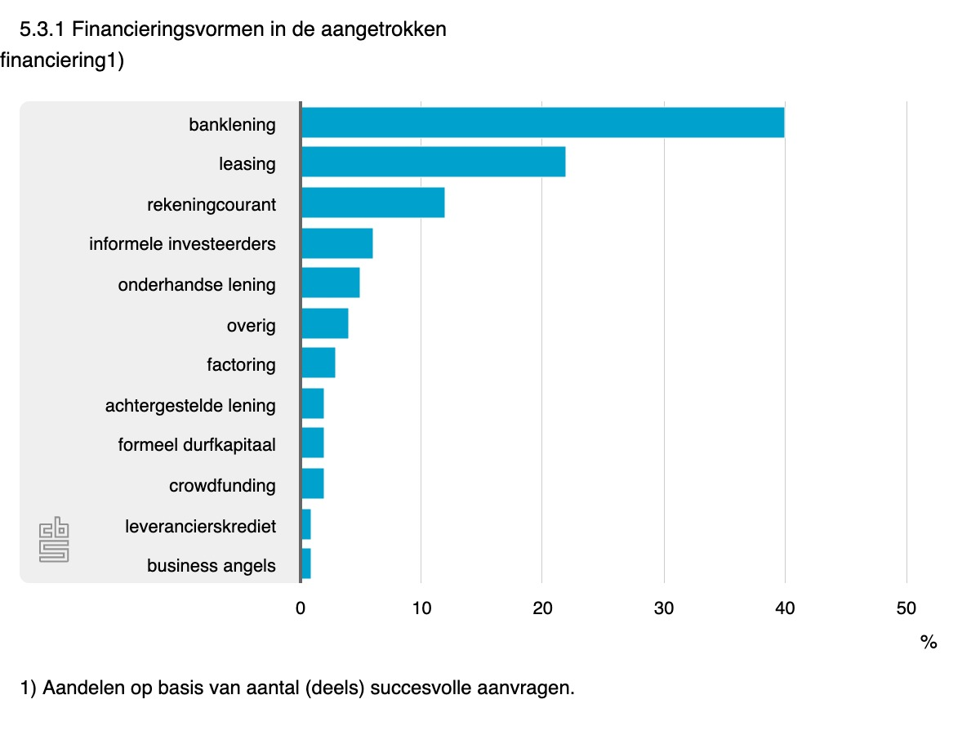

Other forms of financing

In addition to the two basic factoring variants, there are also many other forms of factoring. But factoring is certainly not the only way to obtain funding, as shown in the image below.

Want to know which form of factoring or other financing suits your business? We will be happy to advise you on the right form of financing.